Autocatallaxy

Will Freudenheim | William Morgan | Darren Zhu

Field Statement

From the influence of Thomas Malthus on Charles Darwin to Thorstein Veblen’s coining “evolutionary economics” in “Why Is Economics Not An Evolutionary Science?” (1898), there exists a long history of thinking about the intersection of evolution and economics. In the history of economic thought, this research was picked up during the early and mid 20th century by members of the Austrian and Chicago Schools, namely Schumpeter, Hayek and Alchian. Until the late 20th century, however, these thinkers operated, as Geoffrey Hodgson has suggested, as an “invisible college”, meaning that although some preoccupations of evolutionary economics were shared, the idea had not itself become a grounding principle, a Schelling point, for defining a field of research.

In the late 20th century, this began to change; first with Richard Nelson and Sidney Winter’s An Evolutionary Theory of Economic Change (1982). What Nelson and Winter’s book suggested was, as Phillip Mirowski has commented, “an epoch-making departure from orthodox [neoclassical] theory”, from the maximization function, the well-defined choice set and the choice rationalization of firms. If Nelson and Winter’s work failed to live up to its billing for Mirowski, it nonetheless began the process of formalizing “an evolutionary program” in the history of economic thought.

Enter the Santa Fe Institute (SFI); founded in 1984 as a kind of metascientific school for breaching the disciplinary boundaries of the academy, SFI gathered together the insights of cybernetics, systems theory and computer science under the umbrella header of “the complexity sciences.” In 1995, Doyne Farmer, external professor at SFI since 1986, published the seminal SFI working paper, “Market Force, Ecology, and Evolution.” Therein, Farmer argued for a nonequilibirum price formation rule and a capital allocation model that was equivalent to standard models in population biology. For Farmer and other key SFI thinkers, namely the economist W. Brian Arthur, Herbert Simon’s concept of bounded rationality played a critical role in dismantling the neoclassical assumptions about agents, optimization and price and in forwarding the broad critique that neoclassical economic theory incorrectly assumes a homo economicus model of human behavior. Per Simon, accounts of behavior must include information processing costs, knowledge imperfections, firm and individual irrationality and the ineradicable persistence of novelty and surprise that transform economies from within and without on account of interdependencies and feedback mechanisms.

Given its interests in theorizing complex and nonlinear systems which demonstrate the capacity for spontaneous and adaptive self-organization, it is little surprise that SFI has spearheaded the ongoing revival of Hayekian thought in economics, and also disciplines far beyond. Following Hayek’s “The Use of Knowledge in Society” and The Sensory Order especially, SFI scholars have argued against a physics-based apprehension of the economy, which applies a mechanistic and deterministic framework, arguing instead for a biological framework that is process-dependent and evolutionary.

In 1995, the evolutionary biologists John Maynard Smith (who pioneered the use of mathematics in biology) and Eors Szathmary published the seminal book, The Major Transitions in Evolution, in which they showed how in the evolution of life there have been major transitions in which forms of cooperation emerged leading to higher levels of organization. This thesis, which connected eukaryotes to multicellular organisms to human sociocultural evolution, made it possible to draw a direct line between the evolution of life and evolution in economics. Perhaps unsurprisingly, Maynard Smith was himself personally interested in and visited SFI more than once, at times writing excitedly and others irritatedly about the work being done there.

In the wake of the 2008 financial crisis, evolutionary economics ideas are gaining traction. This project enters the field at this moment. At the same time, however, astro- and xeno-biologists like Sara Walker, Lee Cronin, Michael Levin and Stuart Bartlett are returning to Maynard Smith and Szathmary’s notion of open-ended evolution to consider alternate paths that the evolution of life may have taken, for example on exoplanets or in the evolution of technical systems like AI.

In light of these interventions on the evolutionary biology side, this project revisits the foundations of “life” in economic ecologies, arguing that anthropocentrism has similarly led to misplaced focus on the all too human elements of exchange. Instead it is here argued that price, the informatic medium of exchange, is the true DNA of economics. What price can account for in a given moment, what it can sense dictates the kind of sensory order that is secreted around it. Epistemes and economic systems, capitalism, mercantilism, socialism, are epiphenomena of the major transitions in the evolution of price. Contrary to current evolutionary economic thinking, which maintains a focus on the ecological landscape of firms and strategies, this project argues that price is both what drives and indexes economic evolution, thereby bringing evolutionary economics up to speed with the latest thinking in evolutionary biology.

The intervention of this project arrives at a moment when the self-attention mechanism of transformer models have helped to reignite the Socialist Calculation Controversy of the mid 20th century. In that debate, Hayek “defeated” Oskar Lange and his “socialist cybernetics” by demonstrating that central planning committees failed to continuously integrate information at the speed, flexibility and complexity of markets. Today, economists, scholars and activists, from Daron Acemoglu to Evgeny Morozov to Nathan Robinson are throwing their hats into the ring of the renewed Socialist Calculation Controversy. At the same time, socialist planning is coming back into vogue. This project injects a question into this debate that may be described as a market Turing Test: if an intelligent machine cannot beat the market-machine hybrid at predicting the future, then must price be said to possess intelligence?

Introduction: The Phylogeny of Price

Price is not the number you see at the gas station.

It’s what you don’t see: the sensation, integration, and compression of planetary scale information spread across crude oil prices, refinery markets, OPEC decisions, geopoliticking, distribution and marketing costs, taxes, and the financial instruments layered throughout the network.

If price discovery is indeed an informational process, how did price come to integrate this information and compress it into the numbers we see? Not all at once.

Price has learned its information integration techniques over time. As price’s sensory integration techniques have evolved, so too have the type of economic systems that can be imagined. The level of informational complexity, which price synthesizes is also a measure of the overall complexity of any economy.

Price drives infra-economic evolution; it‘s where “fitness” is meted out—firms die, strategies go extinct, others are born to take their place. The economic systems we know–capitalism, mercantilism, socialism–are not causes, but symptoms of price’s evolving. How price selects for genes of economic fitness reflects the acquired complexity of its sensory order.

If price indeed learns to sense novel information, markets are not so much efficient, as they are adaptive. Following Andrew Lo and the Sante Fe Institute, economics ought not be understood through the lens of physics, but of evolutionary biology.

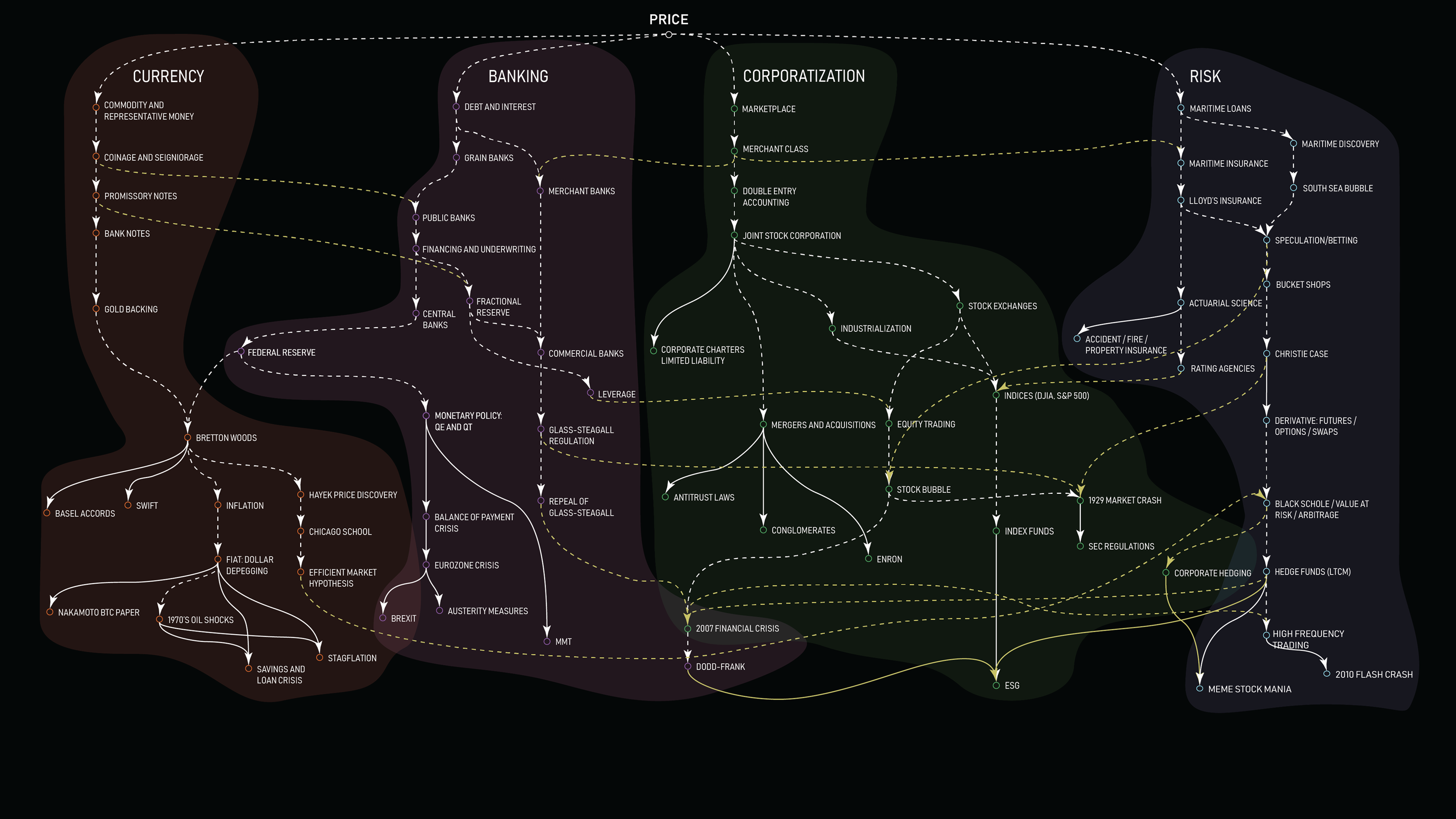

Price’s phylogenetic tree traces its evolutionary history across four key lineages: Currency, Banking, Corporatization, and Risk.

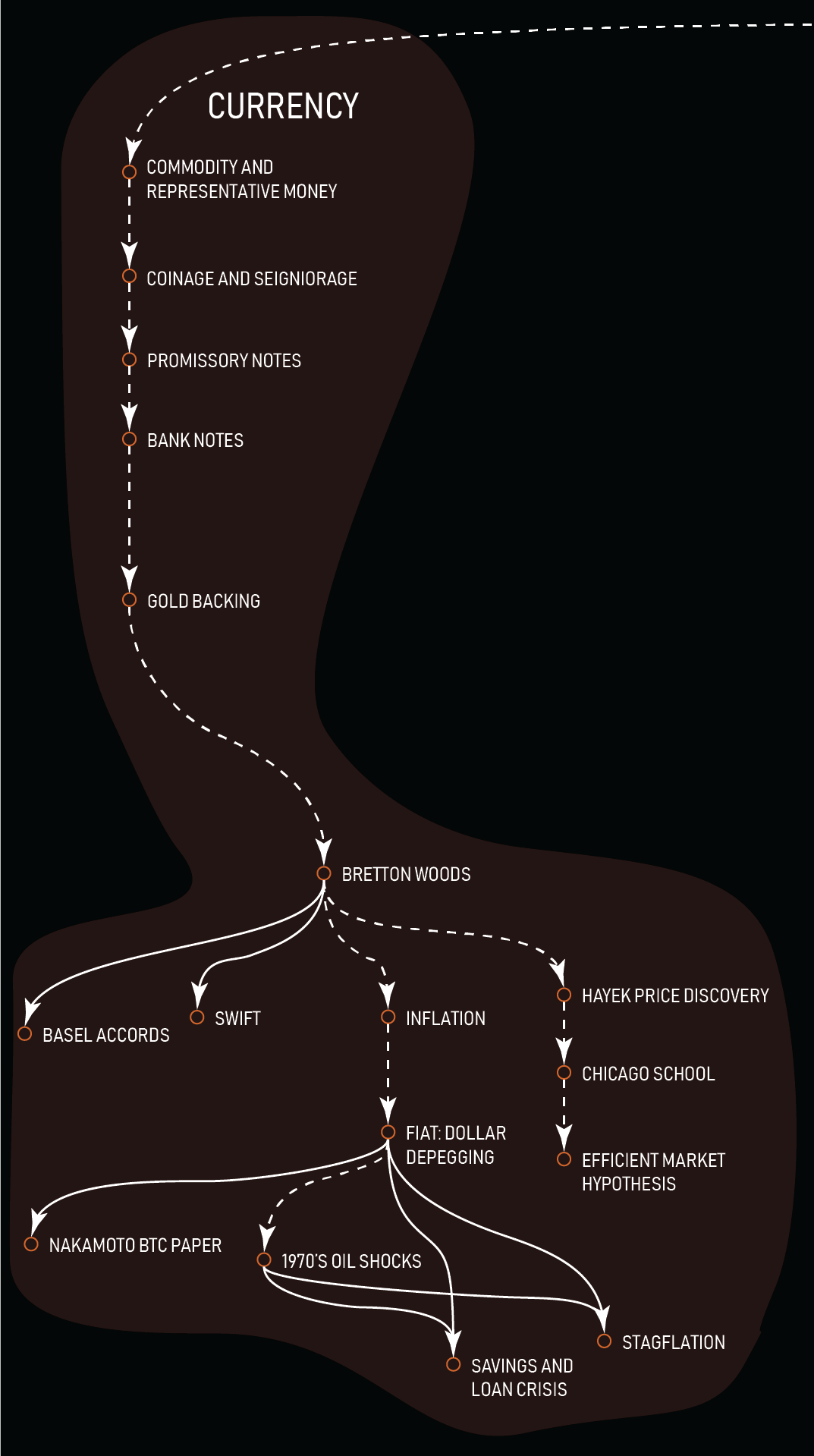

Currency

With currency, price builds a circulatory system, learning how to make value signals interoperable across space and time.

Currency evolves from its commodity to representative form and then becomes legal tender when central banks restrict commercial banks’ right to mint paper. Here, price learns to measure the overall money supply in the system of exchange. In 1971, fearing rising cost of living and insufficient gold reserves, Richard Nixon suspended the dollar’s gold convertibility. Fiat-based currency demanded price’s attunement to signals like Quantitative Easing and Tightening, which create and remove money tout suite.

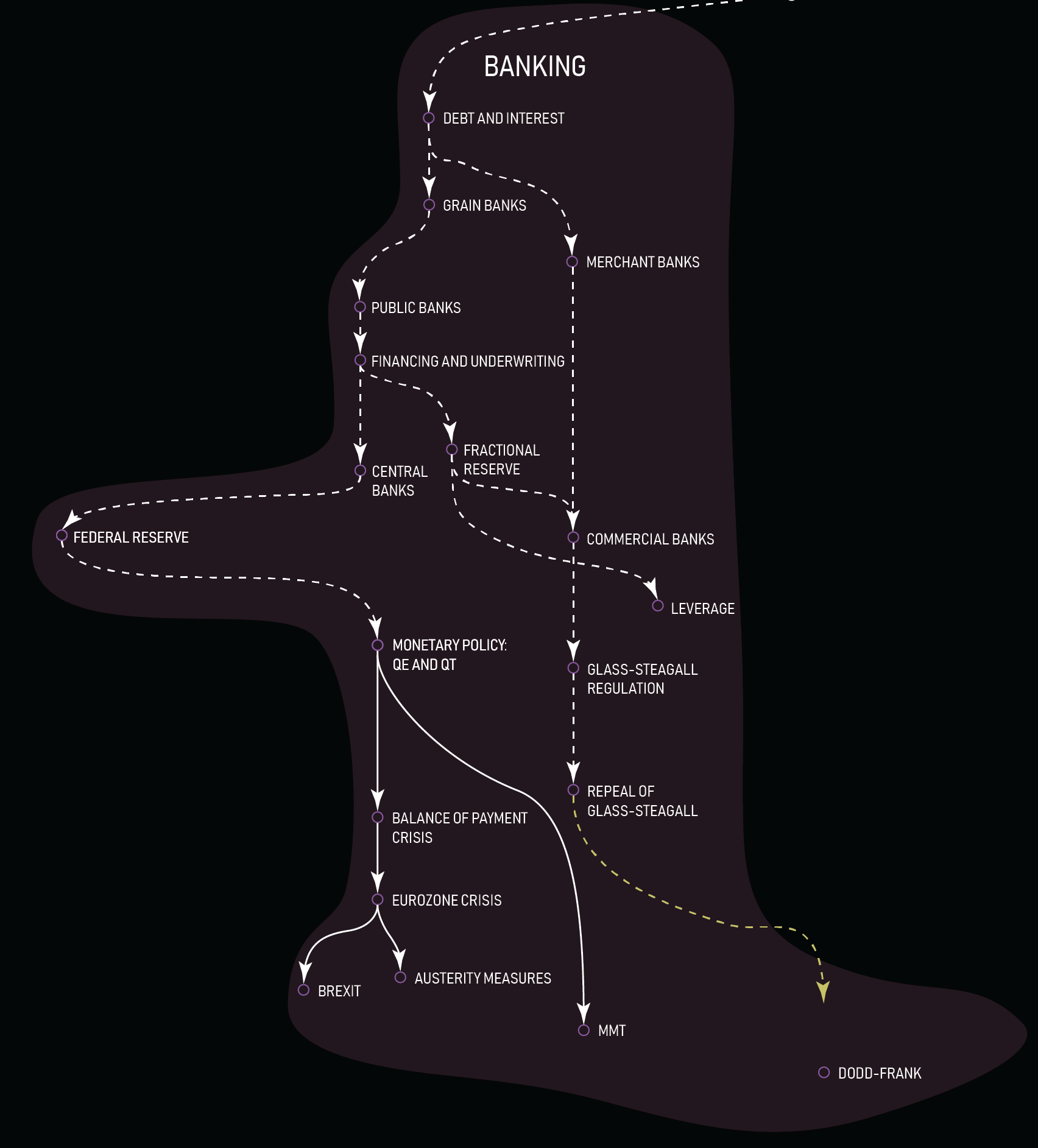

Banking

With banking, price evolves an autonomic nervous system, managing the expansion and contraction of exchange through lines of credit and lenders of last resort.

In 1640, following Charles I’s seizure of private gold, the goldsmiths of London began accepting specie deposits and issuing promissory notes for redemption on demand. Fractional-reserve banking was born as the goldsmiths issued lines of credit leveraged against their reserves, balancing the ratio of assets to capital akin to the evolution of homeostasis. Most recently, central banks formalized mechanisms for maintaining price stability and manipulating money supply: interest rate adjustments, re-financing, and open market operations.

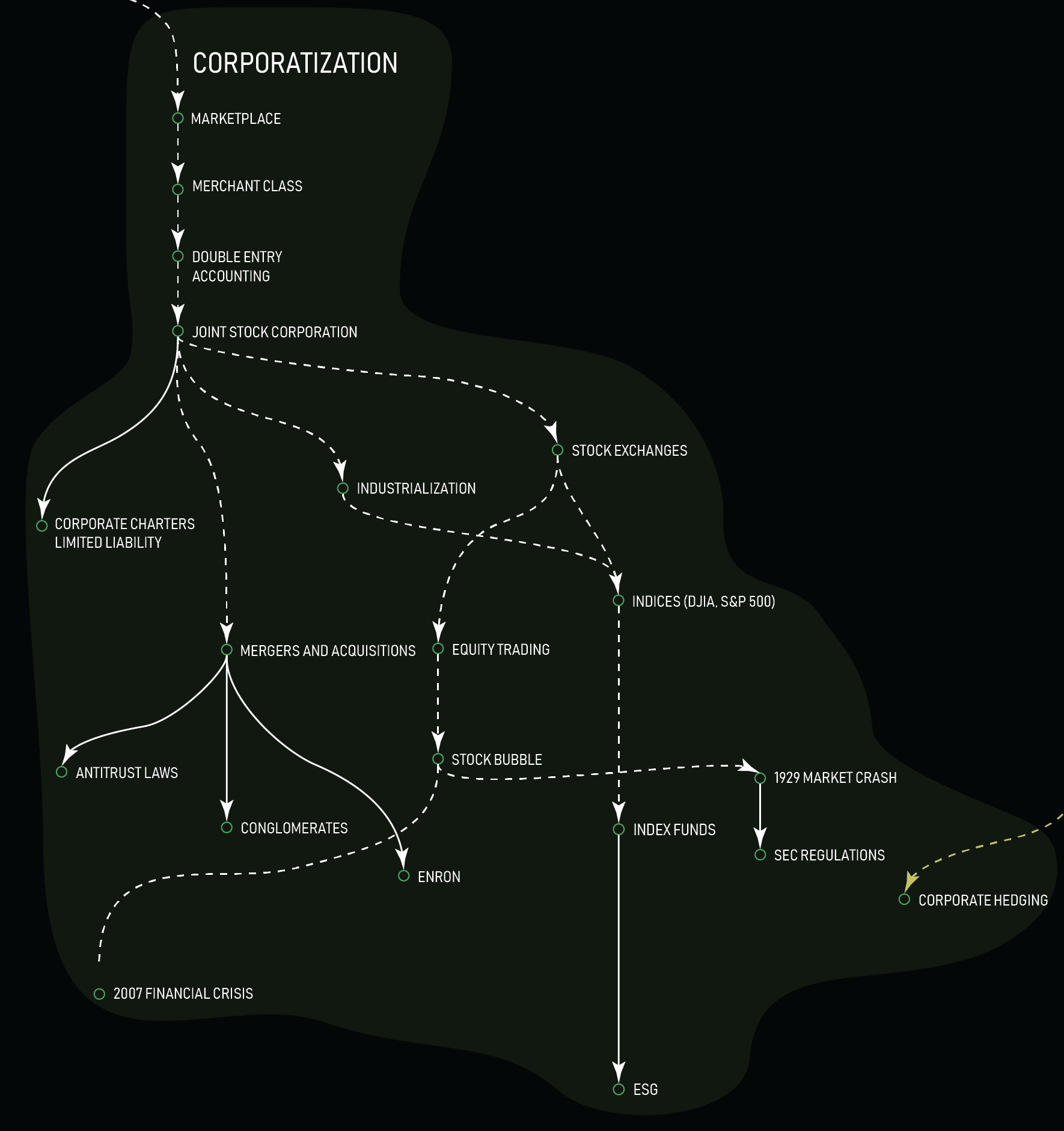

Corporatization

With corporatization, price produced multicellular coordination by learning to value and compel sustained multi-agent collaboration.

In the 17th century, for example, the Dutch and English East India Companies (the first Joint Stock Corporations) raised expedition money by selling stock, allowing investors to share in corporate profits. By the 19th century, corporations obtained legal personhood, abstracting identities from individuals and indemnifying investors against failure. A century later, corporations became conglomerates, cross-industry partnerships under single umbrellas—Disney, Alphabet, Coke.

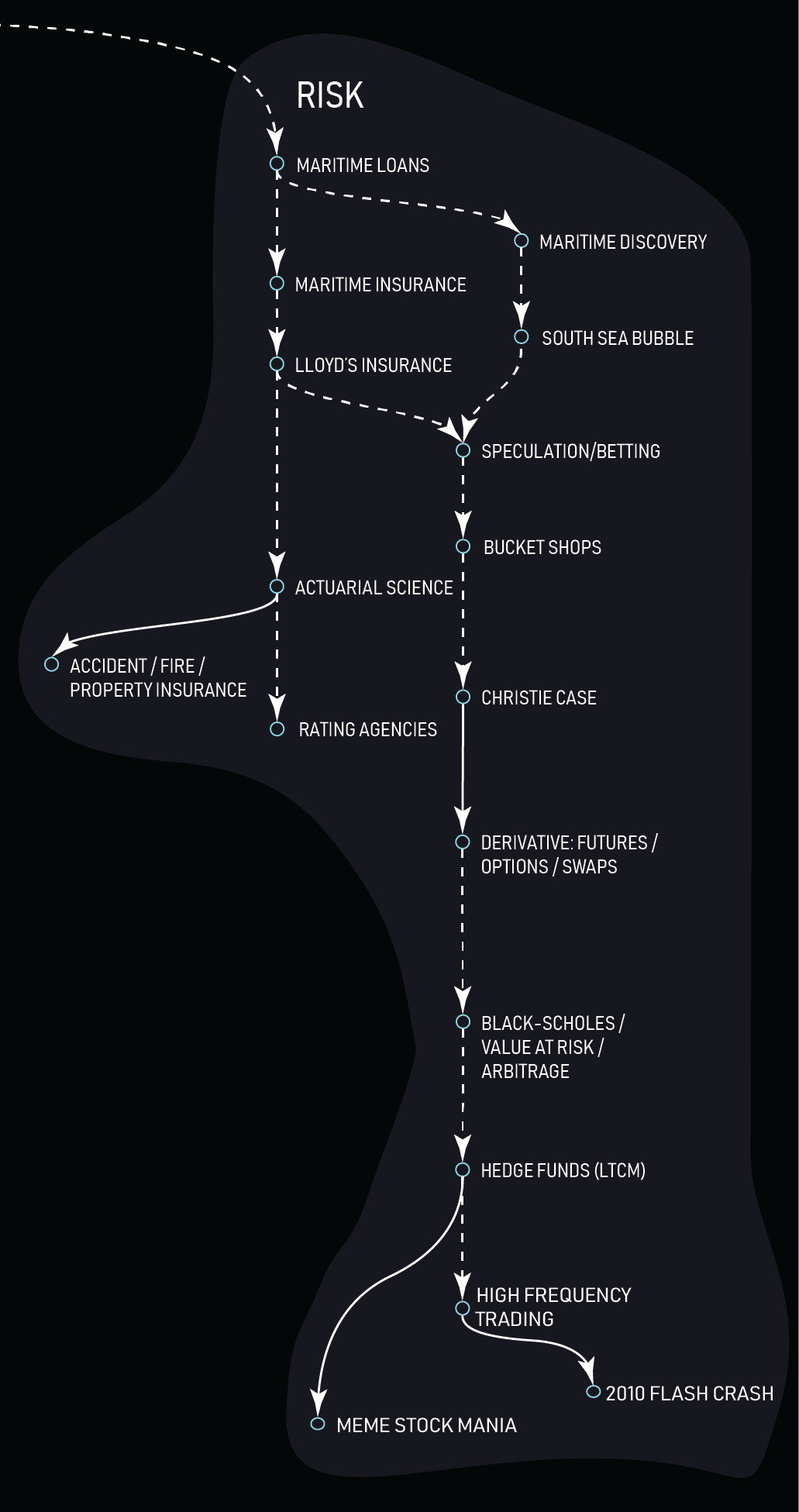

Risk

With risk, as with immune receptors, price evolved mechanisms to negotiate uncertainty.

In the middle ages, Italian city states pioneered early insurance contracts to mitigate the risk of sea voyages and incentivize maritime trade. The resulting distribution of risk led to the flourishing of maritime economies and also facilitated the Age of Discovery. The South Sea Company bubble of 1720 saw stock speculation deployed to tame temporality as martine insurance had been used to manipulate space.

Rather than admonition against pricing time, however, what price learned was the need for greater precision. In the 18th century, Lloyd’s Coffee House emerged as a price nexus: it became an insurance market hub and a site of key shipping information. Merchants gathered to hear the latest news about vessels and to adjust risk allocations. After the US Civil War, where the Union Army had relied heavily upon grain futures to feed its soldiers, widespread speculation became rampant, eventually leading to the Supreme Court’s 1905 Christie Decision, which outlawed bucket shops and codified a professional class of risk managers.

Following the quiet of the post-Depression era, in the early 1970s the modern financial architecture was born: the Chicago Board Options Exchange; Nixon’s de-pegging the dollar; the publication of the Black Scholes formula. These added complexity as mathematical risk management took control with hedge funds like LTCM, arbitrage and Value at Risk. In recent years, Citadel and high frequency traders have come to embody price’s most recent lesson: the more time in a trade, the more risk to manage. A premium has been placed on short term sensing, baking in the potential for shocks.

The Great Carbonization Event

To date, price has evolved enormously complex sensory integration techniques, and as it faces new environmental pressures, its mutation rate is likely to accelerate.

In 2015, Mark Carney, then Governor of the Bank of England spoke at Lloyd’s about “the tragedy of the horizon”: climate change’s catastrophic impacts exceeding individuals’ time horizons.

On the other hand, the time horizon of insurers like Lloyd’s—in operation since 1688—are orders of magnitude larger. Insurers are compelled to calculate future risk. State Farm has already made one such calculation: that climate risks are impossibly unprofitable, hence their discontinuing homeowner’s insurance in California, Florida, Louisiana.

Insurance flight may trigger re-rating of real estate assets—by far the most valuable sector of the economy. Jump-to-distress prices trigger contagions, undermining price stability in businesses’ loan obligations and banks’ capital to asset allocations.

This scenario doesn’t require catastrophes’ unfolding, merely the prediction of one can trigger a metaphorical forest fire in the pricing regime.

A new species of financial instruments may rise to fill the niche vacated by insurers. One such tool combines securitized insurance policies with collateralized loans awarded to climate mitigation and adaptation firms. Establishing the market worth of these products requires the Federal Reserve acting as Buyer of First Resort. Similar to Advanced Market Commitments that funded NASA’s commercial orbital transportation service program (COTS) and Operation Warp Speed’s COVID-19 vaccines, a Fed willingness to inject liquidity into the mega-risk securities market would ignite a ‘green rush,’ triggering the upward re-rating of carbon-based securities as externalities get re-priced as opportunities.

The Great Carbonization Event names this critical juncture in price’s evolution where carbon risks get translocated from ecology into economy.

The Informatic Complexity Threshold

As complexity compounds, price will select for emerging technologies that bolster the adaptive capacities of the global system of exchange.

Today’s mega-risks are born of connection and complexity. A polycrisis rises whose whole is greater than the sum of its parts: pandemic, hemispherical tension, bank failure, energy insecurity, climate catastrophe, information balkanization.

Price will confront this polycrisis and its own role in generating it. What systems will go extinct? What flora and fauna will take their place? Crises precipitate change.

Given the trophic cascade effects of polycrisis risks, it is neither possible nor prudent for consumers to process price signals. Consumer behavior defies neoclassical assumptions: not rational utility maximization, but viral trends, irrational exuberance and panic. Real world behavior layers in volatility in price, magnifying the risk of exogenous shocks, which now find causes in even minor events.

Although consumer irrationality is not new; what is in the polycrisis is the planetary virality of said volatility, its likelihood to set off chain reactions, its unpredictability, its inability to be deterred. In relying on consumers’ interfacing with prices they cannot understand, the world’s developed economies court existential disaster. Consumer economies are maladapted to navigating crises of high dimensional complexity.

Polycrisis produces an Informatic Complexity Threshold in the evolution of price, pressuring it to delink from the consumer economy, relieving individuals of their obligation to act rationally amidst chaos.

“Hypo-pricing” names the process where price lifts off from consumer attention. A precursor exists in the form of digital bundles, such as Spotify’s model of charging consumers flat fee subscriptions. Correspondingly, the bespoke per-stream deals negotiated between artists and labels on the backend represent a subtler and more complex price discovery process that we term “hyper-pricing.”

In hypo-hyper price speciation, economic evolution will incline towards consolidated or distributed modes of price discovery:

- Consolidated: corporations merge into massive conglomerates. For consumers, these novel megafauna or “megaglomerates” operate through hypo-priced bundle fulfillments, a la Amazon Prime but for all goods and services. For suppliers, operations and work flows unfold as hyper-priced negotiations between nested corporations within the megaglomerate.

- Distributed: an open-source or government sponsored “preference protocol” is crafted to match individual consumers with suppliers, of which there are many. Like emails, which are user-owned, but sent and received by different client software, one’s preference profile travels with them and is not owned by any Megaglomerate.

In both models, the hypo-price experience hides price discovery from consumers by matching them to goods and services bundles. Preference inference engines built atop the self-attention mechanism of transformer models alleviate the so-called rational inattention of consumers. Akin to how foundation species reshape environments, novel foundation models push out the consumer economy, the same way that the services species pushed out the industrial economy before it.

Hypo-pricing may evolve to serve as the foundation for a kind of Universal Basic Match. Unlike traditional Universal Basic Income proposals, which provide universal and basic access to the priced economy, what a UBM affords is universal and basic exit from priced exchange and entrance into the matching system.

If one understands contemporary price as being divided between the number consumers see and the information communication work they do not, price’s hypo- and hyper- speciation removes the former entirely. If the price we see is like the tip of an iceberg, hypo and hyper-pricing imply this priceberg’s total submergence into the deep.

Conclusion

Amidst polycrisis, price faces a Great Carbonization Event and an Informatic Complexity Threshold. To survive it must adapt new ways to disclose the risk profile of complex crises, translating them from externalities to opportunities. And to sustain itself, price must evolve past boom-and-bust attention economies: a cladogenesis, an evolutionary divergence from the ancestral democratization of the pricing form into hypo-hyper-priced offspring.

If price succeeds in this delinking, will it set off towards full autonomization? Will its effects be felt like the decrees of a far off sovereign? Could price be described as having intelligence? As having life?

In light of the recent renewal of the Socialist Calculation Debate, consider the Market Turing Test: If an intelligent machine cannot beat the market-machine hybrid at predicting the future, then price must be said to possess intelligence. If the form of price can be shown to have a greater capacity for evolution than a given species, it must be said to possess life.

What gives rise to these questions is the autocatalytic power of price.

References

Burnham, Terence C., And Michael Travisano. “The Landscape Of Innovation In Bacteria, Battleships, And Beyond.” Proceedings Of The National Academy Of Sciences, Vol. 118, No. 26, 2021, E2015565118.

Carney, Mark. “Breaking The Tragedy Of The Horizon–Climate Change And Financial Stability.” Speech Given At Lloyd’s Of London, 29, 2015, Pp. 220-230.

De Goede, Marieke. Virtue, Fortune, And Faith: A Genealogy Of Finance, Vol. 24, University of Minnesota Press, 2001.

Dowling, Bartholomew. Evolutionary Finance. Springer, 2005.

Esposito, Elena. The Future Of Futures: The Time Of Money In Financing And Society. Edward Elgar Publishing, 2011.

Ferguson, Niall. The Ascent Of Money: A Financial History Of The World. Penguin, 2008.

Ferguson, Niall. “An Evolutionary Approach To Financial History.” Cold Spring Harbor Symposia On Quantitative Biology, Vol. 74, Cold Spring Harbor Laboratory Press, 2009.

Halpern, Orit. “Financializing Intelligence: On The Integration Of Machines And Markets.” E-Flux Architecture, March 2023.

Henwood, Doug. “Wall Street.” Capital & Class, Vol. 23, No. 3, 1999, Pp. 167-169.

Levin, Simon A., And Andrew W. Lo. “Introduction To Pnas Special Issue On Evolutionary Models Of Financial Markets.” Proceedings Of The National Academy Of Sciences, Vol. 118, No. 26, 2021, E2104800118.

Lo, Andrew. Adaptive Markets: Financial Evolution At The Speed Of Thought. Princeton University Press, 2017.

Morgan, William R. “Finance Must Be Defended: Cybernetics, Neoliberalism And Environmental, Social, And Governance (Esg).” Sustainability, Vol. 15, No. 4, 2023, Pp. 3707.

Nik-Khah, Edward, And Philip Mirowski. “The Ghosts Of Hayek In Orthodox Microeconomics: Markets As Information Processors.” (2019): 31-70.

Sims, Christopher A. “Implications Of Rational Inattention.” Journal Of Monetary Economics, Vol. 50, No. 3, 2003, Pp. 665-690.

Veblen, Thorstein. “Why Is Economics Not An Evolutionary Science?.” The Quarterly Journal Of Economics, Vol. 12, No. 4, 1898, Pp. 373-397.

Vie, Aymeric, Maarten Peter Scholl, And Doyne James Farmer. “Evology: An Empirically-Calibrated Market Ecology Agent-Based Model For Trading Strategy Search.” Icml 2022 Workshop Ai For Agent-Based Modelling, 2022.

Vodret, Michele. Microfounded Theories Of Price Formation. Diss. Institut Polytechnique De Paris, 2022.

Weyl, E. Glen. “Price theory.” Journal of Economic Literature 57.2 (2019): 329-384.

Whiting, Kate, and HyoJin Park. “This Is Why ‘Polycrisis’ is a Useful Way of Looking At The World Right Now.” Global Health, 7 Mar. 2023.